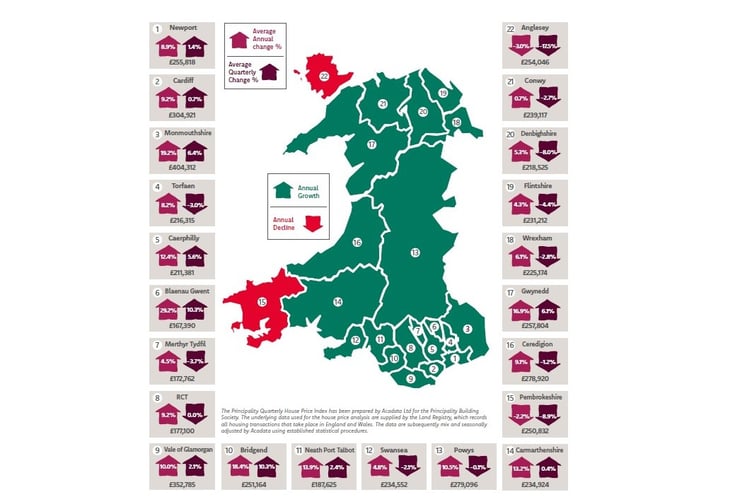

HOUSE prices in Ceredigion have dropped slightly, but still remain nine per cent higher than a year ago, a new study has shown.

Data released by the Principality Building Society shows that Ceredigion house prices dropped by 1.2 per cent in the fourth quarter of 2022, but were 9.1 per cent up on 2021, with the average home now costing £278,920 – nearly £30,000 more than the Welsh average.

Gwynedd saw a 6.1 per cent rise in the fourth quarter of 2022 with prices 16.9 per cent up on 2021, with the average price now standing at £257,804.

Powys recorded an annual rise of 10.5 per cent, with prices dropping 0.1 per cent in the fourth quarter and the average home now costing £279,096.

.jpeg?width=209&height=140&crop=209:145,smart&quality=75)

Carmarthenshire recorded a 0.4 per cent rise in the fourth quarter and annual rise of 13.2 per cent, with an average house price of £234,924.

Only two counties in Wales recorded an annual drop in house prices.

Pembrokeshire recorded an annual 2.2 per cent slump in prices, with an 8.9 per cent drop in the fourth quarter and the average price now standing at £250,832.

Ynys Mon saw a 17.5 per cent drop in the fourth quarter and 3 per cent over the year, with the average price now standing at £254,046 – a drop of more than £50,000 from the third quarter of 2022.

The average house price in Wales for 2022 was £249,076, but cost of living pressures, higher interest rates and stagnant earnings are expected to contribute to a market slowdown.

Despite an almost double-digit price rise – 9.9 per cent - when compared to the same period the previous year nationally, this is the weakest annual price rise in Wales since early 2022 and points towards a more subdued outlook for the housing market in 2023.

This is echoed by a modest 1.3 per cent increase when comparing against the quarter, one of the lowest rates since early 2020 and reinforcing that the strong quarterly rate of house price inflation reported a year ago has dissipated considerably.

Shaun Middleton, Head of Distribution at Principality Building Society said: “Looking back at 2022, Wales has not suffered the more extreme price volatility seen in England. Typically, the housing market was more buoyant than expected partly because of the long-term issue of the shortage of the supply of homes, combined with pent-up demand.

“Matters have improved since the tumultuous mini budget last September, with lenders returning to the market which increased competition and modestly reduced mortgage rates. It does appear that the era of exceptionally low mortgage rates is over. Depending on trends in inflation and the actions of the Bank of England in terms of pushing up the base rate to counter that, we can expect mortgage rates to remain somewhat elevated for the foreseeable future.

“Clearly, there will be a more challenging environment in 2023, with the higher cost of mortgages, rising cost-of-living pressures, plus a further fall in real earnings. These factors will contribute to a slowing market, with house prices widely predicted by analysts to drop slightly. More than 1.4 million households will be coming off much lower fixed-rate loans this year and some could face a payment shock, although the stress tests which have been in place over the last ten years should mean that most mortgaged households will have the capacity to cope with the increase.”

The report estimates that there were about 12,600 transactions in Wales in Q4, up a little on the previous quarter, but about 5% lower than Q4 2021. However, these figures may be somewhat flattered by buyers moving quickly to complete purchases while favourable mortgage deals were available.

For the year as a whole, sales are on a par with levels in 2019, pre-Covid, but noticeably weaker than in 2021- around 12 per cent lower. Much of the decline in sales relates to detached properties (26 per cent lower) and semis (down 12 per cent). Flats are the only property type with a higher volume of sales, albeit with a negligible increase of 1 per cent. This might suggest that affordability pressures are beginning to produce a greater demand for flats.

Comments

This article has no comments yet. Be the first to leave a comment.